What is a Company Voluntary Arrangement (CVA)?

A CVA is an insolvency procedure that allows a company in financial distress that owes money to enter into an arrangement with its creditors to repay its debts, over an agreed period of time. From the commencement of a CVA, a company can continue to trade even though it is insolvent. A CVA can only be supervised by a Licensed Insolvency Practitioner.

Often a company with a seemingly healthy business can find itself with cash flow problems and creditor pressure due to a one-off event. This can lead to it facing insolvency. One such circumstance could be the insolvency of a major customer, a contract going badly wrong, or significant rent increases by landlords. How can we help? Here, a Company Voluntary Arrangement (CVA) is often used to restructure the company and return it to financial health.

Need help?

If your business is facing insolvency, the sooner you contact us, the more we can help.

Learn more about CVAs

When is a Company Voluntary Arrangement used?

A CVA is used if the insolvent company has already or is likely to return to profitability in the near future and the debts can be paid off over an extended period of time. It is in effect a sort of debt-reduction / debt-settlement process, the CVA being a tailored plan to repay the money owed to creditors, usually over a 3-5 year period, based on what the company can afford to pay. Typically, this is between 25% and 60% of the total debt. This gives the company time to reorganise and to turnaround the business.

Take a look at our guide to the Company Voluntary Arrangement process (which includes the main advantages of using a CVA) and scroll down this page for some Frequently Asked Questions. There have been rumblings for reform of CVAs in recent years – take a look at our article about this debate, plus take a look at this article for a comparison of CVAs with Pre Pack Administrations.

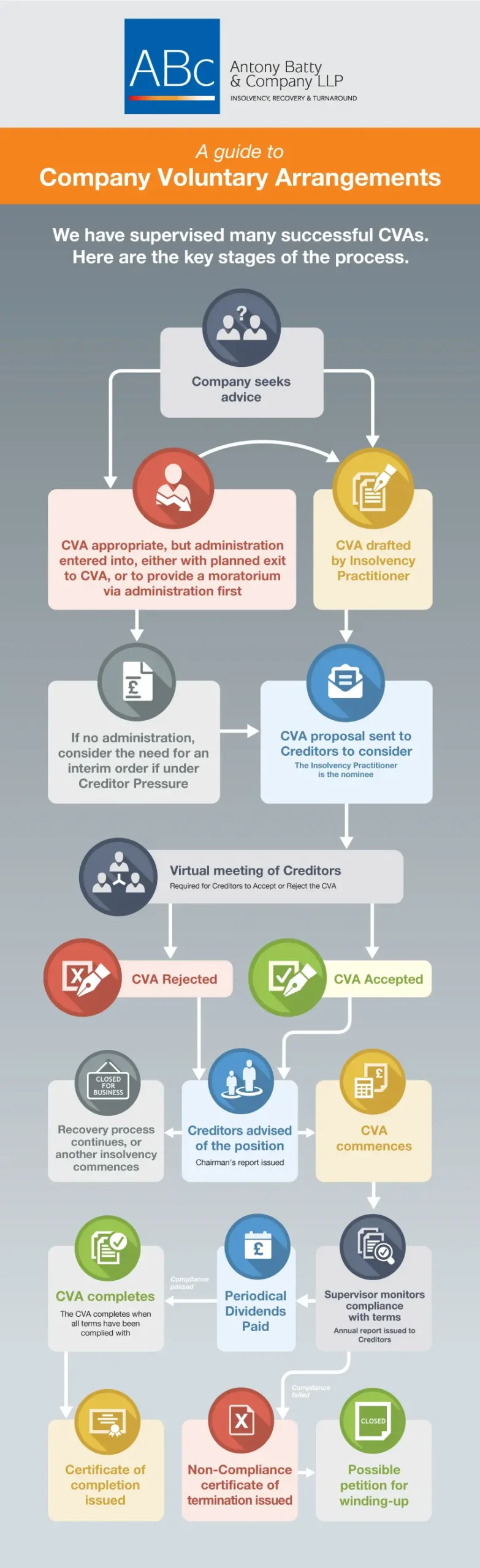

A guide to Company Voluntary Arrangements

How can a CVA help? What are the advantages of a CVA?

A Company Voluntary Arrangement is a contract between a company and its creditors that is legally binding on all concerned. If approached in a proper manner it can give an insolvent business breathing space to resolve its financial problems, take control of, and recover, its financial footing. A CVA offers a very flexible approach to an insolvent situation and, therefore, can be tailor made to your company’s needs.

Get out of debt with a Company Voluntary Arrangement

Initially, an Insolvency Practitioner (IP) is the nominee when a CVA is proposed. The CVA has to be approved by 75% or more (by value) of the creditors. If approved, the IP will become a Supervisor and will enforce the arrangement and become responsible for ensuring the agreed terms are met. If there is an objection or objections to the terms by more than 25% of the creditors (by value), the CVA cannot proceed.

CVA FAQs

If the debtor company does not comply with the CVA’s terms – and it is compulsory that it does so – then:

- The Supervisor may petition for a Company Liquidation through the Courts.

- The creditors of the debtor Company are no longer bound by the terms of the CVA. This means they can pursue debt recovery from the debtor Company for the balance of the debts that are owed.

- The CVA Supervisor must distribute any assets that they hold in partial satisfaction of the company’s debts.

There is no statutory requirement for the Directors to advise their customers that the company has entered into a CVA. However, it may be in the Company’s interest that the Directors are upfront with their customers for the important reason that rumours may spread in the market place that because the Company is insolvent it may be about to cease to trade.

The Directors can explain to the customers that the CVA will enable them to focus on the service they provide rather than concerning themselves with the Company’s financial position. Loyal customers may look to help the company for example by ensuring prompt or early payment for goods and/or services provided.

Key trading partners of the business should be aware of what is going on. A controlled approach to key customers will be much more beneficial than allowing them to hear from Creditors who have received the proposals.

There is no reason why the CVA will prevent a Company from delivering a reliable service. Moreover, it offers the chance for a struggling yet viable Company to continue to satisfy its clients. There is therefore no reason why customers would walk away from a Company that has chosen the CVA route.

Whether the Company decides to inform the customers is the prerogative of the Directors. However, it is important to consider the value of honesty when your customers’ only other sources of information may be your competitors.

Clients will take the view that the new contract is as a result of the quality of the company’s product and or service, but the customer will be checking the Company’s ability to fund itself and to be in business some months or even years down the line. Communication and a controlled approach will usually lead to a positive outcome. Your Insolvency Practitioner will be able to give advice.

Whilst there may be fears that creditors will vote against the proposals, it is often in the best interests of the creditors to work with the CVA process rather than against it. Creditors will ultimately want any debts owed to them to be paid back. More than often, if the business is viable, they will want to continue working with the company. It is important to be honest with the creditors throughout the process.

They will be disappointed, but by proposing a CVA you are showing them that you are trying to continue a business that will maximise the return on current debt to the creditors.

It is all about communication. The best strategy would be to talk to them asserting that the company is seeking to maximise all creditors’ interests by proposing a CVA.

It is likely that some employees will have to be made redundant as part of the process of restructuring and streamlining the business. However, there may be a concern that staff vital to the business going forward may decide to leave.

Generally, they will stay. If they walk out they lose their employment rights and will not receive any redundancy or lieu of notice payments from the company, or the Government should the Company be forced into Liquidation. They may also not be eligible for unemployment/job seekers benefit.

It is our opinion that you must involve employees in a CVA when the time is right, because they are the people who are going to help deliver management’s plans.

If they have a new job to go to there is little to be done to stop disgruntled employees leaving. But if the employees can be involved as part of the recovery – perhaps by offering a share package as part of the long-term strategy the key employees can often be retained.

Again, this is unlikely to happen. If a well-structured plan is used and a well-presented approach to the bank is employed.

Most banks are much more supportive now of “out of court” restructurings like CVAs because they avoid the usual huge asset meltdown and costs of an Administration, for example. Although the CVA cannot affect the rights of the bank or lender, they are stakeholders and should be closely involved in the process.

Then approach the bank. The local branch manager must pass the proposal to his debt recovery unit and cannot (usually) affect the outcome of the deal.

Remember the bank is (usually) secured, therefore the CVA cannot bind the bank legally, but conversion of the overdraft into a longer-term loan may give the bank more comfort that the company is keen to repay the debts. Talk to an Insolvency Practitioner used to dealing with banks, such as Antony Batty & Company.

They are guarantees that cannot be removed unless and until the debt is paid off. The longer-term repayment to secured creditors should be considered as part of the overall restructuring. Once the debt is cleared there is no reason why Personal Guarantees cannot be removed.

A CVA will not lead to these being “called in” as long as a careful plan to deal with secured debt is set out to the lender. Again, banks don’t want to chase people for PGs. They want to lend to responsible and viable businesses.

No. They can be used in future providing they are recognised losses.

Yes there are two methods: one relies on case law and the other is a formal moratorium. For a full explanation of how the new Acts moratorium process works talk to a specialist turnaround practitioner or an insolvency practitioner.

Under case law, providing a creditor has less than 25% of the overall debts of the company then they can be required to consider the proposal even when a winding up petition is issued. A petition may be stayed and adjourned if a carefully structured plan is put together.

If required a CVA can be rapidly prepared to show there is a “reasonable prospect” of the CVA being approved, then the Court will usually adjourn a hearing allowing time for the proposal to be completed and voted on by creditors. This is a complex issue beyond the scope of this guide, but feel free to contact us if you have any questions.

In 1995 case law was reported that provides a very powerful argument. Re Dollar Land (Feltham) & Ors [1995] BCC 740 reported that the court decided that a winding-up order should be rescinded if there was a real prospect that CVA proposals would be approved by the company’s creditors. In other words, let the CVA majority decide.

We use this argument to STOP petitions being issued in the first place, saving the creditor money for costs and fees and also removing the risk of the petition being made against the client.

If a petition is already issued before we have been appointed to assist, and a hearing date is due before we can file the CVA meeting notice, we talk to the petitioner to persuade them to stop their actions, or to prevent the advertisement of the petition.

If the petitioner will not withdraw or threatens advertisement the Company could use an application to Court to request a hearing adjournment and seek a Validation order from the Court saying that the hearing is adjourned and the company can progress the CVA proposal to filing and call a creditors meeting.

An Insolvency Practitioner appointed to supervise the carrying out of a Company Voluntary Arrangement.

TUPE refers to the Transfer of Undertakings (Protection of Employment) Regulations, 2006. TUPE protects the rights of UK employees when a business or service transfers to a new employer.

Looking for an experienced Insolvency Practitioner? We have run over 200 successful Company Voluntary Arrangements

We believe a Company Voluntary Arrangement provides an excellent opportunity for an insolvent Company to survive, clear its business debt and for the creditors and lenders to recover far more of their debt than they would in a Liquidation or through the sale of the assets of the company.

Over the years we have built strong contacts with a number of funders who are willing to inject working capital into a business once its old debts have been ring fenced in a CVA and debt solutions are in place.

Our team of Insolvency Practitioners, in London, Brentwood, Salisbury, Bournemouth and the Thames Valley have used Company Voluntary Arrangements to help over 200 companies that have encountered short-term difficulties. In c.70% of the cases the CVA has allowed them to undertake debt restructuring and reorganisation plans, return the Company to profitability and trade on successfully.